Bitcoin as (part of) your retirement plan

Investing is synonymous with planning for the future, and for most of us, "the future" means retirement. So investing properly means gaming out how to retire not just with enough money to cover your expenses, but enough to truly enjoy every one of your golden years. Here's how Bitcoin can make your old-age planning a little more prosperous.

Key takeaways

- A comfortable retirement usually relies on a few different pillars, a.k.a. diversification; these vary by country

- Like traditional investments, Bitcoin is meant to grow over time

- Unlike traditional investments, Bitcoin offers advantages like higher returns, no contribution limits, and greater portability

What we mean when we talk about retirement planning

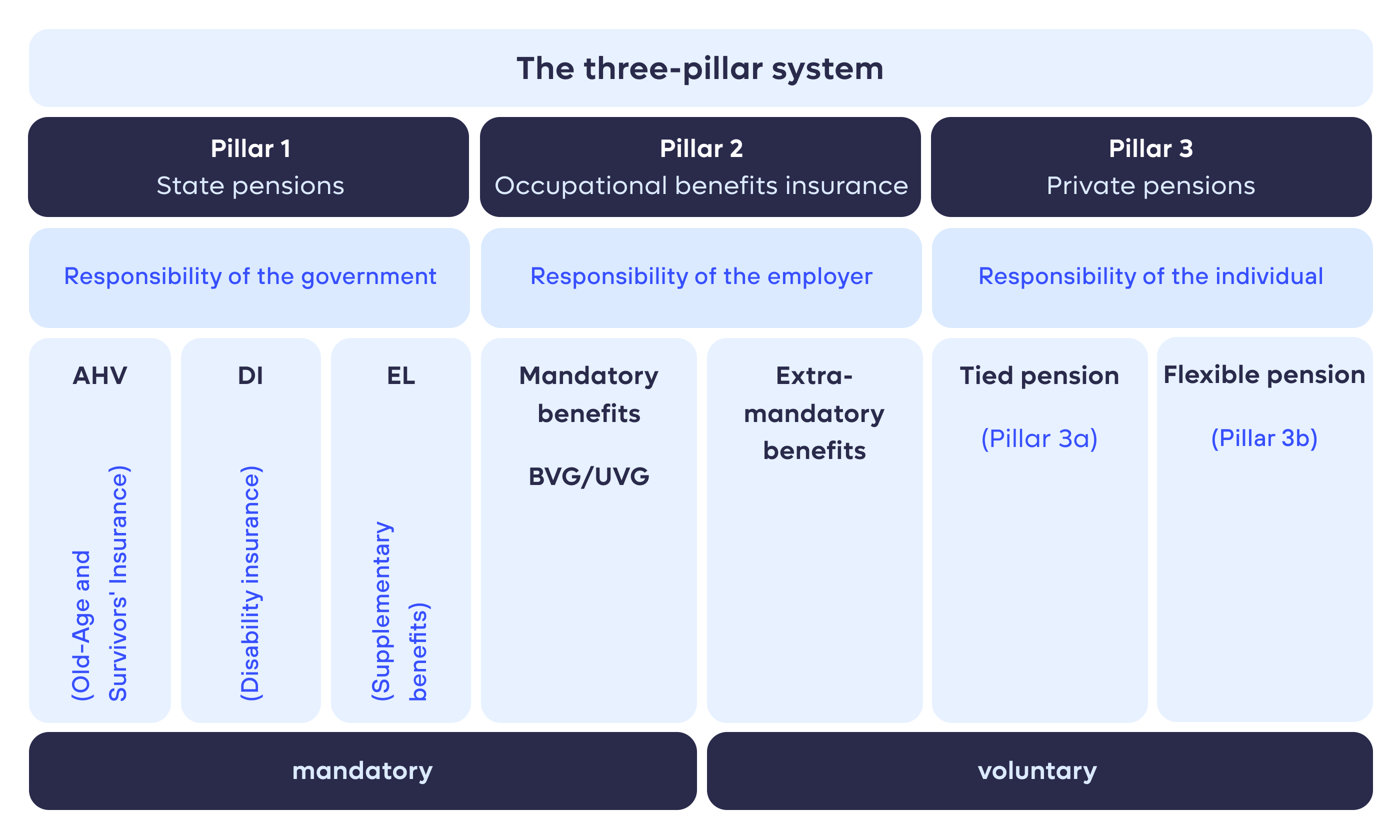

Retirement systems usually rely on a few different pillars, or investing formats. The number and makeup of these pillars varies depending on your country and situation, so—as always—do your own research and remember that Invity doesn't provide financial advice. But there are generally three pillars based on who oversees the funding and payouts: state, employer, and private.

The third pillar is the most flexible, usually including a mix of savings, insurance, individual investments (stocks, ETFs, real estate, etc.), and specialized retirement instruments; a few examples of these are listed below.

- United States: Individual retirement accounts (IRAs), including Roth IRAs, SIMPLE IRAs, etc.

- Germany: Reister Rente

- France: Plan d'épargne retraite (PER)

- Italy: Fondo Pensione Integrativo

Retirement accounts often expose investors to varied investments (e.g. through mutual funds), grow predictably, enjoy government protections, and come with reduced or no taxes if you meet a few criteria. The idea, though, is familiar: pay in throughout your working years, it grows, and you're rewarded later in life.

Drawbacks of a fully traditional third pillar

But even when glossing over issues like inflation, a traditional approach to private retirement planning has some problems. Not fatal ones that mean you should skip it altogether, but serious problems that can limit some of your future flexibility.

For example, the Italian scheme, like an IRA, limits annual contributions to well under €10,000. Yes, the principle you accrue will compound over time, but you'll never be able to maximize your tax-advantaged growth. Got an unexpected bonus one year but already met your limit? Too bad, you'll just have to find somewhere else to put it.

Or take the German plan. If beneficiaries need to tap into their funds before retirement age or want to spend their retirement outside the EU, they must repay all of the subsidies and tax breaks. Say goodbye to chilling on a beach in Tahiti, I guess.

Make the most of your third pillar with Bitcoin

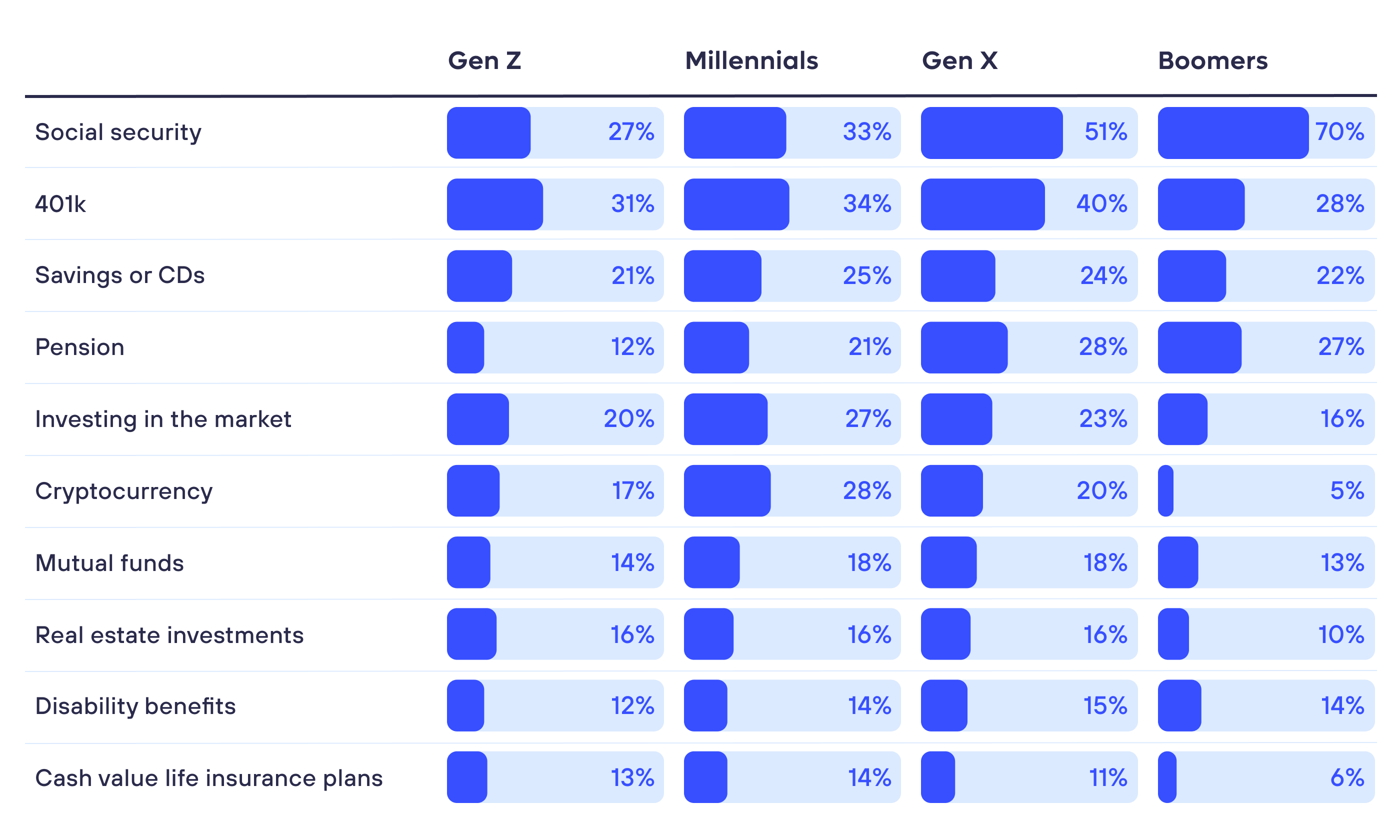

Surprise: Bitcoin fills in a lot of these gaps. This makes crypto a worthwhile complement to traditional approaches to retirement planning. And it's not just us saying so: crypto is more popular than other investment vehicles among young and middle-aged savers, and Bitcoin is even being mainstreamed as part of 401(k)s in the US.

Higher returns

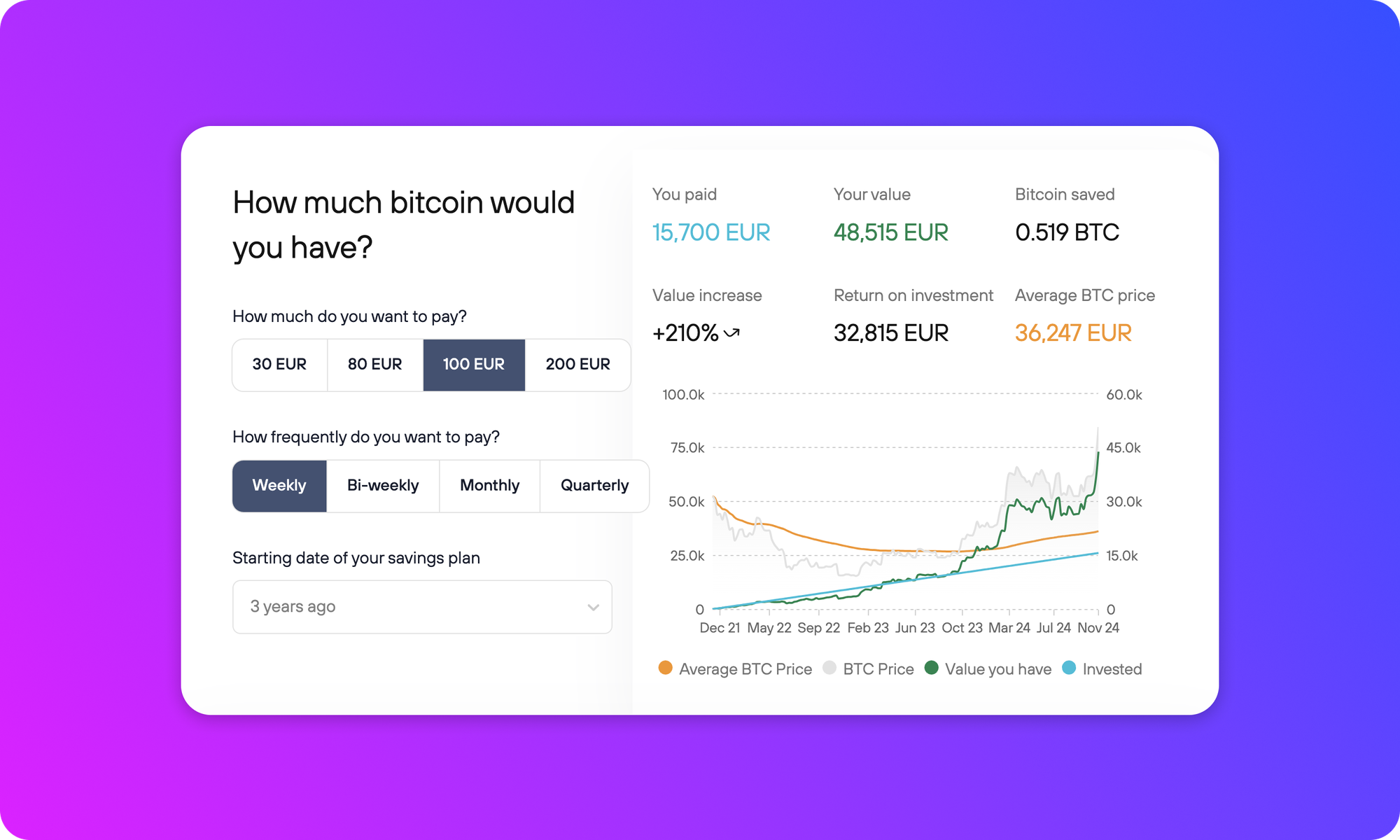

Returns are the most obvious place Bitcoin has a leg up. Even with its volatility, Bitcoin's annual returns average out to around 50%, well in excess of a good index fund's 10%, and dollar-cost averaging can help even out the peaks and valleys. Don't believe me? Invity's dollar-cost averaging calculator provides some pretty striking real numbers.

If you started from zero and invested €100 every week for three years into Bitcoin, you would have spent €15,700 in fiat; this is roughly in the neighborhood of three years of max contributions to an Italian Fondo Pensione Integrativo. With Bitcoin, you would end up with a cool €48,515, while 10% returns in a retirement account with the same approach would get you…€18,307. Before fees. Oof.

See how your own BTC investment strategy stacks up here .

Try Invity mobile app for one-time and recurring bitcoin purchases:

No max contributions, no penalties

But let's forget about maximum contributions altogether—Bitcoin doesn't have them. Since BTC is self-managed, you can buy as little or as much as you like, when you like.

And if life gets rocky and you need to tap into your reserve? Selling some sats from time to time likely just means paying some taxes on realized gains, rather than back taxes that jeopardize your whole savings. Take that, Reister Rente.

Extreme portability

Finally, once it comes time to kick back, Bitcoin, like your retirement dreams, is borderless. It doesn't matter if you're staying close to the grandkids, taking that long-awaited cruise, or living that tropical life—you can sell your Bitcoin for fiat online from anywhere, find someone who wants to buy or trade Bitcoin, or you can simply use your sats as a payment method.

Best of all, you can do all of the above right in the Invity app. Set up recurring buys, hodl on for years to come, and cash out when the time is right, all from the comfort of your smartphone. Download or check in on your nest egg today!